Below are given

back testing results of V2, generated by the back testing software. These results should be considered as

extrapolation into the past of V2 - Volatility Trading Program, which started

live trading on December 1, 2015. Performance fees (20% of new net profit

above high water mark) are not deducted from back testing results.

To see actual trading results, please go to the Performance page.

Back testing results

can be found in this spreadsheet.

Results do take into account bid/ask spreads and negative interest on borrowed

equity (sold short).

V2 Features:

- The back testing history goes back 60 months (the entire available history of the traded instruments was used),

and the results for this strategy are very promising. The variability of returns is low and the

Sharpe Ratio is excellent. The strategy is extremely robust i.e. relatively insensitive

to parameter changes (it is not a curve fitted, or over optimized

system), which usually anticipates excellent performance in forward trading,

following the back testing period.

- Transaction costs are very low (only 1.8% of

net asset value per annum), relative to average annualized rate of return

(around 10% per annum). These calculations are based on a $100,000 test account.

In larger accounts, the efficiency should be somewhat better.

- The strategy trades

liquid instruments (VXX and XIV ETNs) and has moderate capacity. The unavailability to sell

short stock at certain times was not taken into account.

- The strategy is minimally affected by price

slippage, as it trades liquid trading instruments and makes relatively small

position adjustments during the trading day. Hence, the actual trading results are very close to hypothetical

results. See "Transaction costs" above.

- V2 has relatively shallow drawdowns and, due to

the excellent profitability in back testing, the strategy should recovers

relatively fast.

- Back testing results do take into account the

interest paid on "hard to borrow" shares. As of November 2015 the average interest

on open positions was around 4.4% per year at Interactive Brokers.

- Larger annualized returns can be obtained by

employing portfolio margin and additional leverage in accounts funded in excess of $100,000 (with

Interactive Brokers).

V2 -

HYPOTHETICAL PERFORMANCE REPORT FROM STRATEGY BACK TESTING

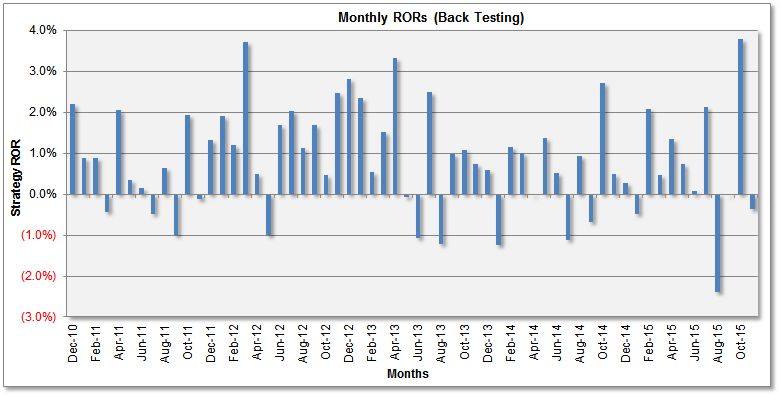

1. Monthly Rates

of Return (ROR), Before Performance Fees

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Total

VAMI

2010

-

-

-

-

-

-

-

-

-

-

-

2.21%

2.21%

1,022.1

2011

0.88%

0.89%

(0.44%)

2.06%

0.34%

0.15%

(0.48%)

0.64%

(1.00%)

1.93%

(0.13%)

1.33%

6.29%

1,086.4

2012

1.91%

1.21%

3.71%

0.50%

(1.00%)

1.70%

2.03%

1.13%

1.68%

0.48%

2.48%

2.81%

20.22%

1,306.1

2013

2.34%

0.55%

1.53%

3.33%

(0.08%)

(1.06%)

2.50%

(1.21%)

0.99%

1.09%

0.74%

0.59%

11.80%

1,460.3

2014

(1.24%)

1.16%

1.01%

(0.01%)

1.36%

0.52%

(1.12%)

0.93%

(0.68%)

2.71%

0.50%

0.28%

5.48%

1,540.4

2015

(0.48%)

2.09%

0.46%

1.34%

0.74%

0.08%

2.13%

(2.40%)

(0.02%)

3.78%

(0.36%)

-

7.47%

1,655.4

2. Performance

Statistics, Based on Back Testing Results (Before Performance Fees)

Strategy Returns (Before

Performance Fees)

Testing

period (60 months)

Dec/2010 -

Nov/2015

Net profit on fixed capital

without/with monthly profit reinvesting

Average annual transaction

costs - bid/ask spreads and commissions and negative

interest (deducted from annual ROR)

6% of NAV

per annum

Average transaction bid/ask spread

and commission cost, as a fraction

of the transaction value (already taken into account)

0.06%

More back testing results, for the three

strategies (V1, V2, V4) combined are available upon request.

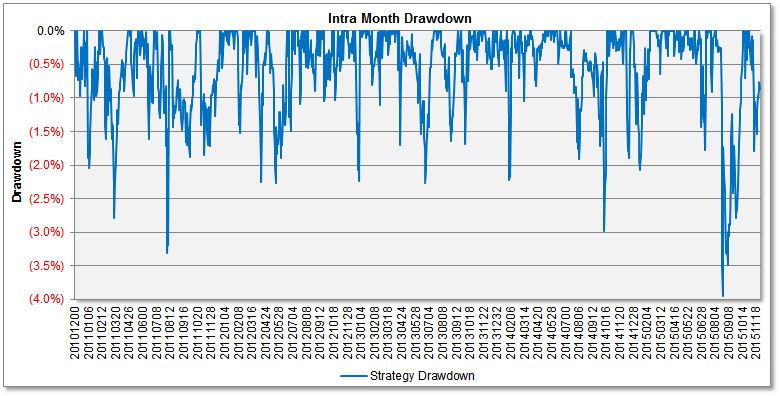

PLEASE ANALYZE AND

THOROUGHLY UNDERSTAND THE RISK / DRAWDOWN PARAMETERS ABOVE AND THE DRAWDOWN

CHART BELOW BEFORE YOU DECIDE TO INVEST IN THE PROGRAM. AS WITH ANY TRADING

PROGRAM, THERE IS NO GUARANTEE THE SYSTEM WILL NOT EXCEED THE WORST DRAWDOWN

FROM THE PAST. WE DO NOT RECOMMEND INVESTING MORE THAN 1/3 OF YOUR TOTAL

INVESTMENT PORTFOLIO IN ANY PARTICULAR PROGRAM, INCLUDING V1D - VOLATILITY

TRADING PROGRAM.

3. Performance Graphs

Monthly Rates of Return (ROR, before

management fees)

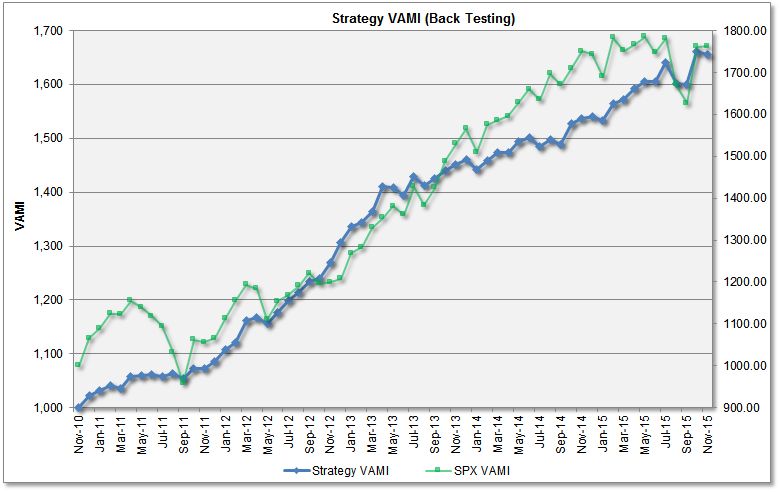

Monthly

Strategy VAMI vs. S&P 500 Index

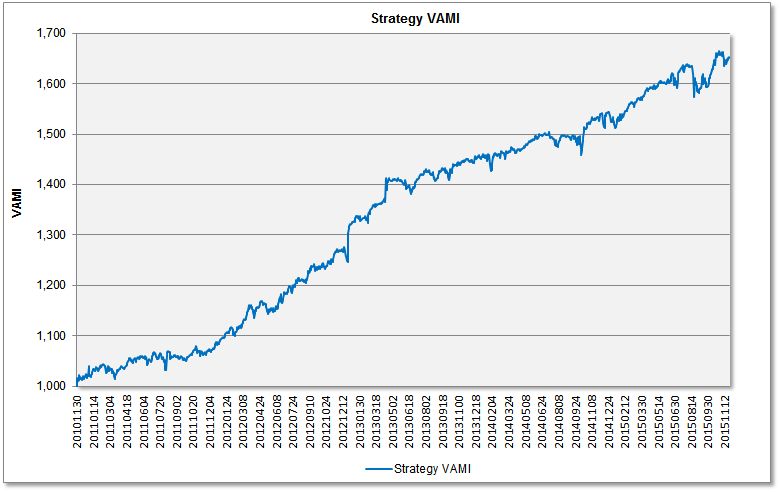

Daily Strategy VAMI vs. S&P 500 Index

Intra-Month Drawdown

Compoundingis an efficient method for increasing your account

equity exponentially, by reinvesting the profit (see the VAMI charts above

and

try this

Financial Calculator).

You can see these

formulas for ROR

calculations and compounding.

The above

tables and charts document V2's historical hypothetical performance

based on back testing results. To see

actual trading results, please go to the Performance page.

Please note

that performance results reported are before performance fees, which

decrease returns. Interest on open positions is not taken into account in

hypothetical results. There may also be slight differences in profit/loss on

different trading platforms.

HYPOTHETICAL OR

SIMULATED PERFORMANCE RESULTS HAVE CERTAIN INHERENT LIMITATIONS. UNLIKE AN

ACTUAL PERFORMANCE RECORD, SIMULATED RESULTS DO NOT REPRESENT ACTUAL TRADING.

ALSO, SINCE THE TRADES HAVE NOT ACTUALLY BEEN EXECUTED, THE RESULTS MAY HAVE

UNDER-OR-OVERCOMPENSATED FOR THE IMPACT, IF ANY, OF CERTAIN MARKET FACTORS, SUCH

AS LACK OF LIQUIDITY. SIMULATED TRADING PLATFORMS IN GENERAL ARE ALSO SUBJECT TO

THE FACT THAT THEY ARE DESIGNED WITH THE BENEFIT OF HINDSIGHT. NO REPRESENTATION

IS BEING MADE THAT ANY ACCOUNT WILL OR IS LIKELY TO ACHIEVE PROFITS OR LOSSES

SIMILAR TO THOSE SHOWN.

Risk Disclaimer

THE RISK OF

LOSS IN TRADING EQUITIES AND ETFS CAN BE SUBSTANTIAL. YOU SHOULD THEREFORE

CAREFULLY CONSIDER WHETHER SUCH TRADING IS SUITABLE FOR YOU IN LIGHT OF YOUR

FINANCIAL CONDITION AND INVESTMENT OBJECTIVES. PAST PERFORMANCE IS NOT

NECESSARILY INDICATIVE OF FUTURE RESULTS. THE PERFORMANCE QUOTED REPRESENTS PAST

PERFORMANCE AND CURRENT PERFORMANCE MAY BE LOWER OR HIGHER. TRADING EQUITIES IS

SPECULATIVE AND MAY INVOLVE THE LOSS OF PRINCIPAL; THEREFORE, FUNDS PLACED UNDER

MANAGEMENT SHOULD BE RISK CAPITAL FUNDS THAT IF LOST WILL NOT SIGNIFICANTLY

AFFECT ONE'S PERSONAL WELL BEING. THIS IS NOT A SOLICITATION TO INVEST AND YOU

SHOULD CAREFULLY CONSIDER YOUR FINANCIAL SITUATION PRIOR TO MAKING ANY

INVESTMENT OR ENTERING INTO ANY TRANSACTION. PLEASE SEE THE COMPLETE

RISK DISCLOSURE.